Northrop Grumman Savings Plan

The Northrop Grumman Savings Plan (NGSP), a 401(k) plan, allows eligible employees to contribute and invest for their financial future, so they can achieve their retirement savings goals.

Employees may contribute from 1% to 75% of their eligible compensation in 1% increments up to IRS limits before taxes are withheld (pre-tax contributions) and/or after taxes are withheld through Roth 401(k) contributions or regular after-tax contributions to the Northrop Grumman Savings Plan (NGSP) unless they’re considered highly compensated under IRS rules. Contributions from highly compensated employees are limited to 35%. Contributions may be made on a tax-advantaged basis, roth 401(k) or after-tax basis up to IRS limits. Read more about saving plan limits below.

In addition to the contributions they make to their NGSP, employees are eligible to receive a matching contribution from Northrop Grumman. Matching contributions occur each pay period the employee contributes to the plan.

You can contribute from 1% to 75% of your eligible compensation in increments of 1%. Highly compensated employees can contribute a maximum of 35%. You can make the following types of contributions:

-

Pre-tax: Before taxes are withheld from your paycheck and taxed along with related earnings at the time of distribution.

-

Roth 401(k): After taxes are withheld from your paycheck, but related earnings are tax-free on qualified distributions.

-

After-tax: After taxes are withheld from your paycheck. Only related earnings on these contributions are taxable at the time of distribution.

-

Any combination of the three.

View the NGC Contribution Comparison Chart for more details.

New and rehired eligible employees are automatically enrolled in the Northrop Grumman Savings Plan (NGSP). Approximately 45 days after your hire or rehire date, 4% of your eligible pay will automatically be deducted on a pre-tax basis and your contribution rate will be increased automatically by 1% each year, unless you elect to change those options.

To review or change your contributions or investment elections, visit Fidelity NetBenefits.

Company Match

Northrop Grumman will make a matching contribution based on the sub-plan in which you participate. To determine your sub-plan, log in to NetBenefits to view the NGSP Summary Plan Description (SPD).

Other Company Contributions

Depending on your hire date and employment history, you may receive an annual company Non-Elective Contribution (NEC) or Retirement Account Contribution (RAC). To determine your NEC or RAC eligibility, log in to NetBenefits to view the NGSP Summary Plan Description (SPD).

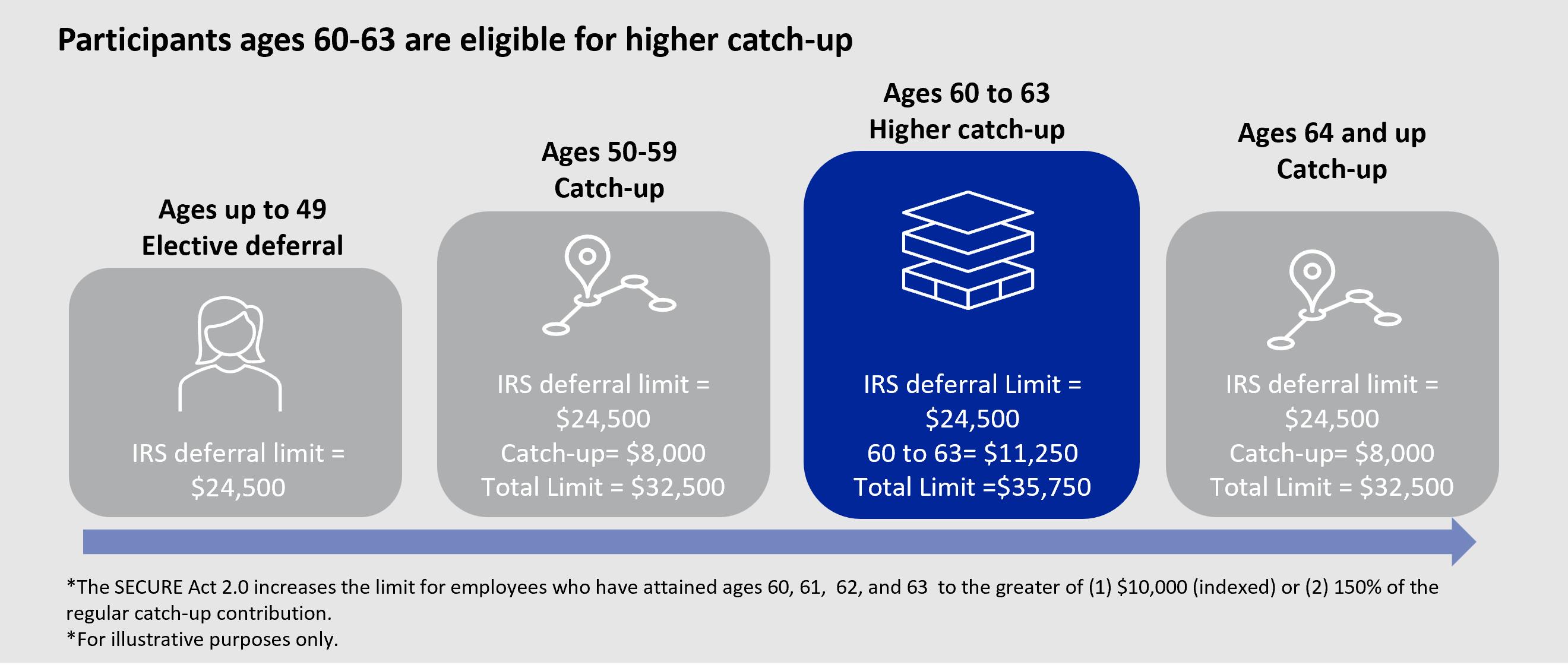

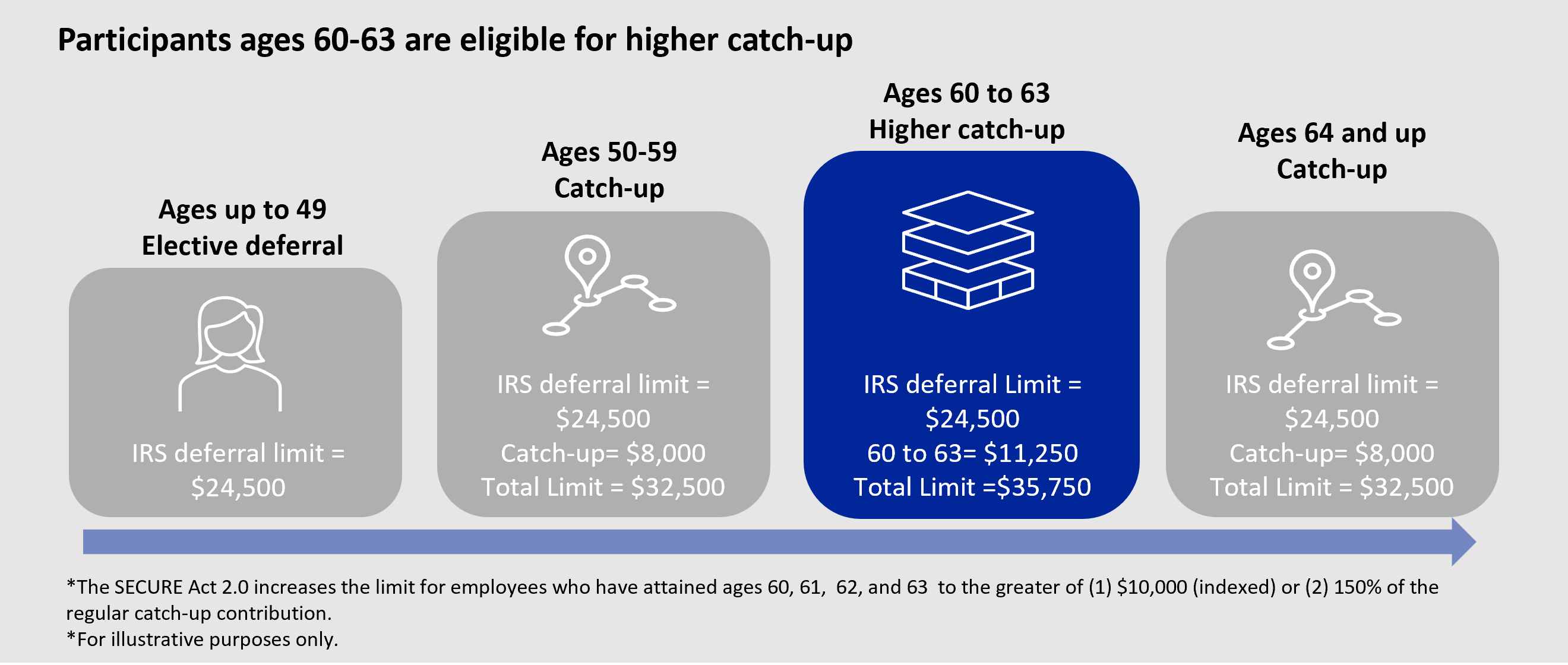

If you’re age 50 to 59 or 64 and older, you can make catch-up contributions of up to $8,000 to help you save more for retirement.

The catch-up contribution for individuals age 60 to 63 is $11,250 for 2026. This higher catch-up limit is only available during the calendar years in which you turn 60 to 63. After that, regular limits apply, so don’t miss out.

The IRS sets limits, based on your age, on the amount you’re allowed to contribute to your Northrop Grumman Savings Plan (NGSP).

The NGSP does not require a separate election for catch-up contributions. If you would like to take advantage of the catch-up contribution feature, you will need to take action by increasing your pre-tax and/or Roth 401(k) contribution rate(s) to the desired amount above the $24,500 contribution limit.

Starting in 2026, the SECURE 2.0 Act requires a change for high-income earners aged 50 or older. If your FICA wages (Box 3 on your W-2) for 2025 exceeded $150,000, any catch-up contributions in 2026 must be made as Roth and not pre-tax.

View resources

| 2026 IRS Contribution Limits for Pre-tax and Roth 401(k) | |

| Under age 50 | $24,500 |

| “Catch-up” amount for age 50 and over | $8,000 |

| “Catch-up” amount for age 60 to 63 | $11,250 |

| Total Contribution Limit | $32,500 |

You will need to do the math to determine the appropriate percentage (in whole numbers only) to elect for your contribution rate(s) to reach your desired contribution total. For example, if you want to contribute the $32,500 maximum contribution and your eligible compensation is $100,000:

*For a definition of eligible compensation, please refer to the NGSP Summary Plan Description on NetBenefits.

** This example assumes you begin, and continue, the contribution rate on the first paycheck of the year.

Savings Contribution Limits

Part of planning for retirement includes contributing to the Northrop Grumman Savings Plan (NGSP). Below are the savings plan contribution limits as defined by the IRS.

|

2026 IRS Savings Plan Contribution Limits |

If You Under Age 50 |

If You're Age 50 or Older* |

If You’re Age 60-63** |

|---|---|---|---|

|

Your Pre-tax and/or Roth 401(k) Contribution Limit |

Maximum of $24,500 (up from $23,500 in 2025) |

Additional $8,000 in catch-up contributions, for a maximum of up to $32,500. (up from $31,000 in 2025) |

Additional $11,250 in catch-up contributions for a maximum of $35,750 |

|

Limit on total contributions (your pre-tax, Roth 401(k) and after-tax contributions plus Northrop Grumman's contributions) |

100% of annual pay or $72,000, whichever is less (up from $70,000 in 2025) |

100% of annual pay or $80,000 ($72,000 + $8,000 in catch-up contributions), whichever is less (up from $77,500 in 2025) |

100% of annual pay or $83,250 ($72,000 + $11,250 in catch-up contributions), whichever is less |

*You must be at least 50 years old by the end of 2026 to be eligible to make catch-up contributions in 2026.

**The catch-up contribution limit for individuals age 60 to 63 is $11,250 for 2026. This higher catch-up limit is only available during the calendar years in which you turn 60 to 63. After that, regular limits apply, so don’t miss out.

Note: In 2026, the total annual amount of eligible compensation on which your NGSP contributions may be based is the first $360,000 (up from $350,000 in 2025) of earnings. Pay above this limit can't be deferred into the NGSP plan.

The Northrop Grumman Savings Plan (NGSP) offers three different investment approaches to help you reach your savings and retirement goals:

- Option 1 (NGSP Retirement Path Funds): Let a professional investment manager design and manage an investment portfolio for you based on your target retirement age. These are considered as part of the core fund line-up.

- Option 2 (NGSP Core Funds): In addition to the NGSP Retirement Path Funds, there are eight other core investment fund options you can choose from to balance your risk and reward potential.

- Option 3 (Brokerage): Build and monitor your own investment portfolio with several core investment fund options and the Fidelity BrokerageLink.

To review your contributions, balance and investments, visit NetBenefits.

Note: Trading restrictions apply to the core funds. See the SPD for details.

You're immediately 100% vested in your employee contributions. You're generally 100% vested in any company contributions after three years of service.

Loans:

Employees may generally borrow up to 50% of their vested Northrop Grumman Savings Plan (NGSP) account, up to legal limits. The portion of the account that's being borrowed won’t make any investment gains while out of the plan.

Withdrawals:

If employees experience financial hardships, they may request a withdrawal of a portion of their account while still working at Northrop Grumman. Be sure to understand both the tax consequences and implications for long-term savings of taking a withdrawal.

To learn more about the loan and withdrawal options, visit NetBenefits or call the Northrop Grumman Benefits Center (NGBC) at (800-894-4194

How Much Money Will You Need to Retire?

|

If you want this amount of income each year of your retirement... |

Your retirement nest egg must be...* |

||

|---|---|---|---|

|

$20,000 |

$233,800 |

$279,400 |

$304,400 |

|

$40,000 |

$467,600 |

$558,700 |

$608,800 |

|

$60,000 |

$701,400 |

$838,200 |

$913,200 |

|

$80,000 |

$935,200 |

$1,117,500 |

$1,217,700 |

|

|

...to last 20 years |

...to last 30 years |

...to last 40 years |

*Figures reflect the assumption that your nest egg grows 6% a year. Beyond the number of years shown, your account balance is $0. The ending values don't reflect taxes, fees or inflation. If they did, amounts would be lower. Taxes will be due upon withdrawal. Distributions before age 59 1/2 may also be subject to a 10% penalty. The assumed rate of return used in this example isn't guaranteed.

A Comfortable Retirement Is Within Your Reach

Saving enough for retirement takes your entire career. With a long-term goal like that, it can be a challenge to stay on track, especially with so many competing priorities. However, small steps over time can really add up. Fidelity recommends you save at least 15% of your income, including company contributions, toward retirement. Below are additional tips for you and your family.

The first step to getting your savings on track is to know where your money's going. Make a list of all your monthly income and expenses and, if you haven’t already, add "Savings Plan." Write down the amounts. Then you can see what you do ― or can save and ― invest each month. Putting the amount in writing can help you achieve two important results: First, you’ll start thinking of saving for retirement as an important financial obligation. Second, you’ll feel more committed to following through on your savings budget.

Now that you have your list, deduct the total from your monthly income. Are you already contributing at least 15% toward your retirement? If not, money left over after taxes could be your chance to chip in a little more! If there’s nothing left over after taxes, it might be time to review your expenses and see if there’s anything you can do without. If you’re already contributing 15%, perhaps you want to contribute a bit more or even consider your other savings priorities, like building an emergency fund.

Consider Automatic Contributions

One of the best ways to save for any goal – especially retirement – is to contribute straight from your paycheck before you have a chance to spend it. With automatic contributions, you can do just that. If you're already contributing, are you able to maximize your contributions to get the most out of the company match?

Remember, Northrop Grumman matches based on your combined pre-tax, Roth 401(k) and after-tax contributions made each pay period.

Push Your Perspective (The Power of Compound Interest)

Saving for retirement is a long-term goal. For some of us, it can be hard prioritizing retirement over something immediate today. If you feel like saving is a sacrifice, you're not alone. How would it feel to push your perspective and make saving a treat?

Fidelity recommends you save at least 15% of your income for retirement. For some people, that means weighing some “wants” against that long-term goal to get to 15%. Now, we’re not talking about things you need ― like food, housing and health care ― or even a little treat like Friday night pizza. We’re talking more about the “shiny things” that have you reaching for your wallet before thinking (and we’ve all been there).

Pushing your perspective is easy, but it takes practice. The next time you see something you wish to purchase, ask, “What will this $100 look like in 20 years?” If you invest that same $100 in your retirement savings with an average annual return of 6%, it will more than triple in value. Now, what if you did this every month, and instead of making a purchase you invested in your future? If you invest an extra $100 a month in your retirement savings, at an average annual rate of 6%, it will look like $16,470 after 10 years and $46,435 after 20 years. Now that’s a treat.

Get Help If You Need It

A financial planner or advisor can help you establish a clear retirement savings goal, help you decide how much to contribute to the Northrop Grumman Savings Plan (NGSP) and other investments (like an Individual Retirement Account or IRA) and help you choose an investment mix that’s right for your personal situation. If you’re approaching retirement, a professional can also help you decide when and how to start taking distributions from the NGSP.

Fixed-fee financial planners may charge for their services, but many investors think having an expert opinion is worth it. Encouragement and advice from a financial planner may be just the motivation you need to get your savings in shape.

Have you ever asked yourself "Am I contributing enough to the Northrop Grumman Savings Plan (NGSP)?" "Have I selected the right investments?" "Will I have enough to retire?"

The Fidelity Personalized Planning and Advice service is available to Northrop Grumman Savings Plan (NGSP) participants. This service gives you access to a team of professionals who can help you create and maintain an investment strategy. You can get the support you need to put your plan into action and track your progress against your goals. Please note there's an advisory fee for this optional service.

For more information, visit the investments section of NetBenefits.

Fidelity Personalized Planning & Advice at Work is a service of Fidelity Personal and Workplace Advisors LLC and Strategic Advisers LLC. Both are registered investment advisers, are Fidelity Investments companies and may be referred to as "Fidelity," "we," or "our" within. For more information, refer to the Terms and Conditions of the Program. When used herein, Fidelity Personalized Planning & Advice refers exclusively to Fidelity Personalized Planning & Advice at Work. This service provides advisory services for a fee.

Links to external sites listed are provided for informational purposes only. Northrop Grumman is not responsible for and doesn't specifically approve or endorse any of the content or any advertisements that, may be found or accessed on these websites.

Fidelity NetBenefits

The NetBenefits website offers information about your Northrop Grumman Savings Plan (NGSP), including investment options and portfolio performance. The site is available virtually 24/7 and among many things, it allows you to easily change your NGSP contribution rate or investment funds, and designate or update your beneficiary(ies).

-

The Planning & Guidance Center helps you analyze where you are towards saving for a goal — and set a clear plan of action to get you where you want to be. Choose whether you want to plan for retirement, college or other financial goal, or for an overall investment strategy. You can then enter your information to determine your situation and objectives, and see the impact on your goals by changing key assumptions and modeling different scenarios.

-

In addition, there are other planning tools and resources available. From budgeting and debt management, to buying a home and saving for college, you can find information to break it all down—and next steps to help you get, and stay, on track. Go to the Learn Hub section on NetBenefits to tips, tools and resources on a multitude of financial topics.

AARP Retirement Calculator

Some of the features in this retirement calculator include the ability to develop a retirement plan for a dual-income home, the ability to calculate and include individual Social Security benefit estimates as a part of retirement income, an explanation of where an individual currently stands in their retirement planning and the ability to experiment with various retirement scenarios to create a plan for every situation.

America Saves

A nationwide coalition of non-profit, corporate and government groups encouraging saving and providing resources and strategies for paying down debt, saving for retirement and building wealth.

Choose to Save

Developed by the Employee Benefit Research Institute (EBRI) through its American Savings Education Council (ASEC) program, Choose to Save is a national public education and outreach program dedicated to raising awareness about the need to plan and save for long-term personal financial security. The site offers a wide variety of savings calculators for creating a budget, saving for a home or college and retirement planning.

MyMoney.gov

MyMoney.gov contains tools and resources for personal financial planning and is offered by the U.S. Financial Literacy and Education Commission.

Savings Fitness: A Guide to Your Money and Financial Future

The U.S. Department of Labor and Certified Financial Planner Board of Standards Inc. (CFP Board) partnered to provide information to help you succeed in setting financial and retirement goals. This booklet starts you on the way to setting savings goals, avoiding savings pitfalls and putting your retirement high on your list of personal priorities.